是否可以用google的搜尋紀錄統計資料來預測金融市場?

參考資料:

DOI: 10.1002/for.2446

Fima在1965年時提出的市場效率理論(market efficiency theory)闡述了市場參與者在時間t接受到市場訊息並在時間t+k內做出交易決策進而影響市場價格。現在由於網路的資訊取得容易,市場資訊很容易被量化研究,例如在google上搜尋”感冒症狀”的頻率較高的地區代表該地區正爆發感冒疫情的可能性較高.把這個理論用在金融市場上就像是投資人在t時的情緒低落會影響到t+k時的交易決策,而投資人在t時的情緒低落也會影響到投資人在t時對於某些關鍵字的搜尋頻率.因此,我們觀察某些關鍵字在t時的搜尋頻率增加可以用來預測t+k時投資人可能會採取的交易行為.

2011年時Bollen等人研究了投資人在Twitter上留言的情緒(冷靜,警覺,恐慌,快樂)與金融市場價格的有相關性.2012年時Bordino等人發現商品的交易量與商品的搜尋頻率成正相關.同年Da等人發現某商品的搜尋頻率指標(search volume index)與某商品在兩週內會獲得正報酬呈現正相關.在2013年時Preis等人利用Google Sets研究有98個關鍵字搜尋頻率(例如: 債卷, 債務, 投資...等)與股票市場呈現極度的相關性.該篇論文認為可以利用這些字的收尋頻率做交易決策,研究中發現關鍵字”債務”對於行情的影響性最大.

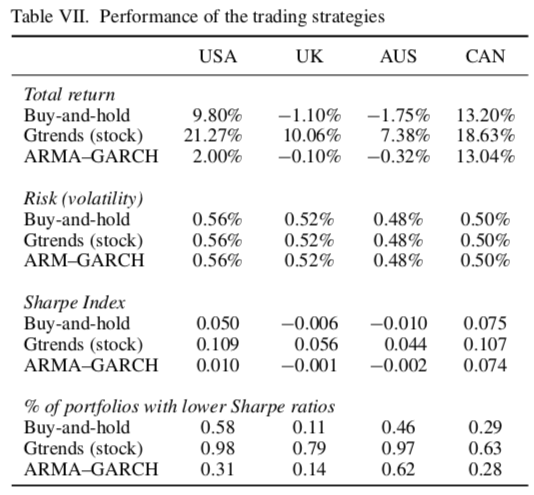

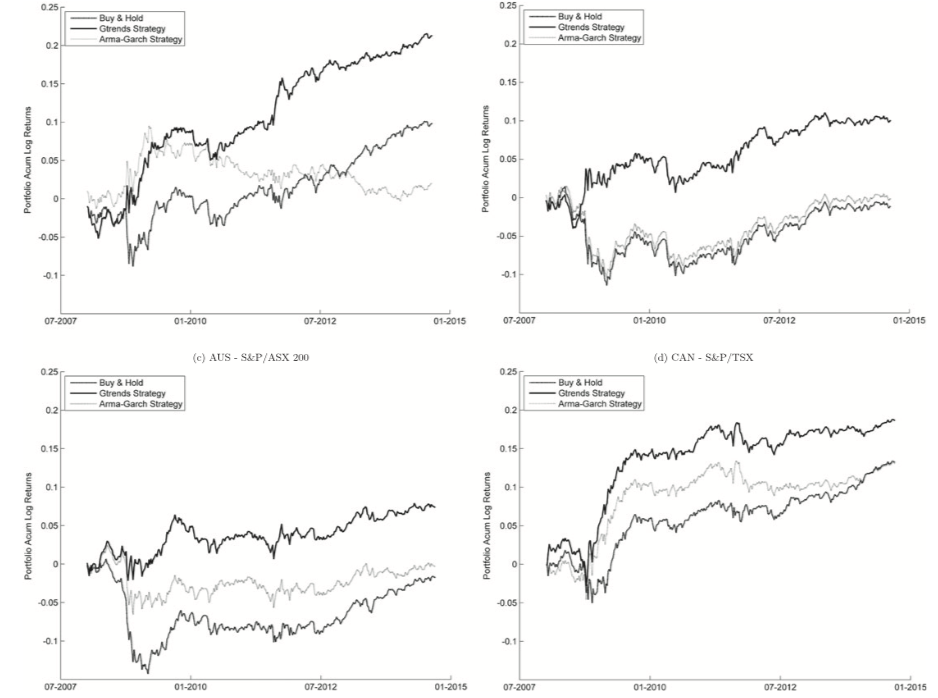

Perlin等人在2016年利用統計學的向量自迴歸模型(VAR model)將google trends對特定財金相關單字的搜尋頻率與市場行情(log報酬率, 波動性, 交易量)的相關性做出對未來有較高報酬率的交易決策。這個方法不僅適用於美國還適用於英國,澳洲和加拿大.此google trend的交易策略比買進不賣(buy and hold)與自回歸條件異變異數模型(ARCH model, Autoregressive conditional heteroskedasticity model)的報酬率還要高出許多且風險波動性變化不大.其中Perlin還發現投資人習慣在賣出股票前在google上搜尋關鍵字stock, 因此stock關鍵字的搜尋頻率與股票負報酬有正相關性.

表一 不同交易策略與其對應的報酬率,波動性,夏普值

圖一 不同交易策略與其對應的報酬率(a) USA—S&P 500; (b) UK—FTSE; (c) AUS—S&P/ASX 200; (d) CAN—S&P/TSX

參考資料:

1. Fama EF. 1965. The behavior of stock-market prices. Journal of Business 38(1): 34–105.

2. Fama EF. 1970. Efficient capital markets: a review of theory and empirical work. Journal of Finance 25(2): 383–417.

3. Bordino I, Battiston S, Caldarelli G, Cristelli M, Ukkonen A, Weber I. 2012. Web search queries can predict stock market volumes. PloS One 7(7): e40014.

4. Bollen J, Mao H, Zeng X. 2011. Twitter mood predicts the stock market. Journal of Computational Science 2(1): 1–8. Da Z, Engelberg J, Gao P. 2011. In search of attention. Journal of Finance 66(5): 1461–1499.

5. Preis T, Moat HS, Stanley HE. 2013. Quantifying trading behavior in financial markets using Google Trends. Scientific Reports 3: article 1684.

1. Fama EF. 1965. The behavior of stock-market prices. Journal of Business 38(1): 34–105.

2. Fama EF. 1970. Efficient capital markets: a review of theory and empirical work. Journal of Finance 25(2): 383–417.

3. Bordino I, Battiston S, Caldarelli G, Cristelli M, Ukkonen A, Weber I. 2012. Web search queries can predict stock market volumes. PloS One 7(7): e40014.

4. Bollen J, Mao H, Zeng X. 2011. Twitter mood predicts the stock market. Journal of Computational Science 2(1): 1–8. Da Z, Engelberg J, Gao P. 2011. In search of attention. Journal of Finance 66(5): 1461–1499.

5. Preis T, Moat HS, Stanley HE. 2013. Quantifying trading behavior in financial markets using Google Trends. Scientific Reports 3: article 1684.